- Get link

- X

- Other Apps

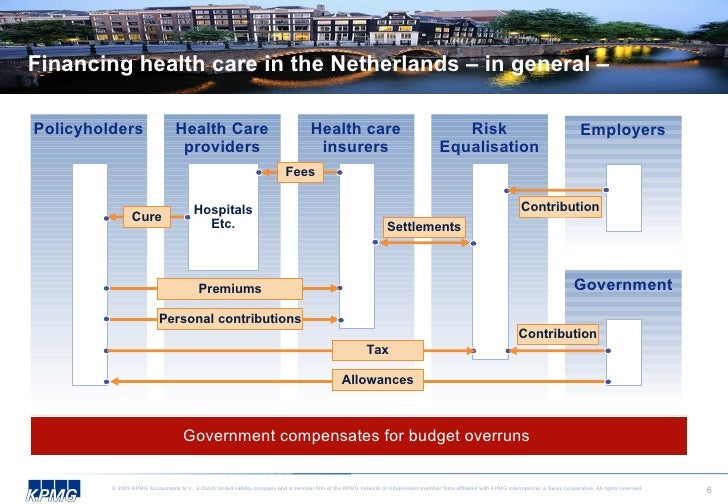

In the year 2006, in the Netherlands an all new system of insurance of health came into force. This all new system of health insurance very truly avoids the two pitfalls of moral hazard and adverse selection that is really associated with the traditional forms of insurance of health by using a combination of an insurance equalisation pool and regulation.

Each and every insurance company, agency and provider very truly receive funds from the equalisation pool mainly to help cover the price of this coverage that is very truly government-mandated. This equalisation pool is very truly run by a regulator which collects income-based contributions from each and every employer, which makes up almost around 60% of all health care funding.

The remaining 40% of the health care funding very truly comes from the insurance premiums that is paid by the public, for which the health insurance companies, agencies and providers compete on cost, though the variation between all the various different competing insurers is only around 3-4%.

However, all the insurance companies, agencies and providers are totally free to sell additional policies of health insurance to very truly provide coverage beyond the national minimum. All these policies do not very truly receive funding from the equalization pool, but cover treatments that are really additional, such as physiotherapy and also dental procedures, which are not at all paid for by the mandatory policy.

Also it is also very well known that high-risk individuals very truly get much more from the pool and low-salary people and also the children under the age of 18 years have their insurance paid for entirely. Because of this reason, the health insurance agencies, companies and agencies no longer find insuring the high risk individuals, and thereby avoiding the adverse selection which is very truly a potential problem.

Insurance companies, agencies and providers are very truly not at all allowed to have co-payments, deductibles, caps, or to deny the coverage to a person who is applying for a policy of health insurance

, or to charge anything other than their published standard premiums.

, or to charge anything other than their published standard premiums.

Comments